14 min read

"Community Group Buying: Why Giants Are Rushing into This Market for a Few Bundles of Cabbage"

This article is Lu Canwei's 28th original piece.

Recently, the People's Daily published a commentary titled "Behind the Controversy of 'Community Group Buying' is Greater Expectation for Technological Innovation from Internet Giants," which mentioned that the accumulated data and algorithms of the internet, besides monetizing traffic, have another way to open up, which is to promote technological innovation. It calls on internet companies not to just focus on a few bundles of cabbage.

So what exactly is community group buying, and how does it differ from group buying? If it's about buying vegetables, can't Meituan and Dingdong buy vegetables solve the problem? Why is there still hype around community group buying? Is it merely a change in internet concepts without any real difference, or is it a new trend?

First, I see that public opinion online is overwhelmingly one-sided. Meanwhile, SpaceX next door is busy launching rockets, and Tesla's market value is skyrocketing. Yet our giants are fixated on cabbages and radishes, even trying to profit from the vegetable money of small vendors. I won't delve into such philosophical questions here, but why are internet giants willing to spend money to seize this market? For now, I won't draw conclusions; you can continue reading.

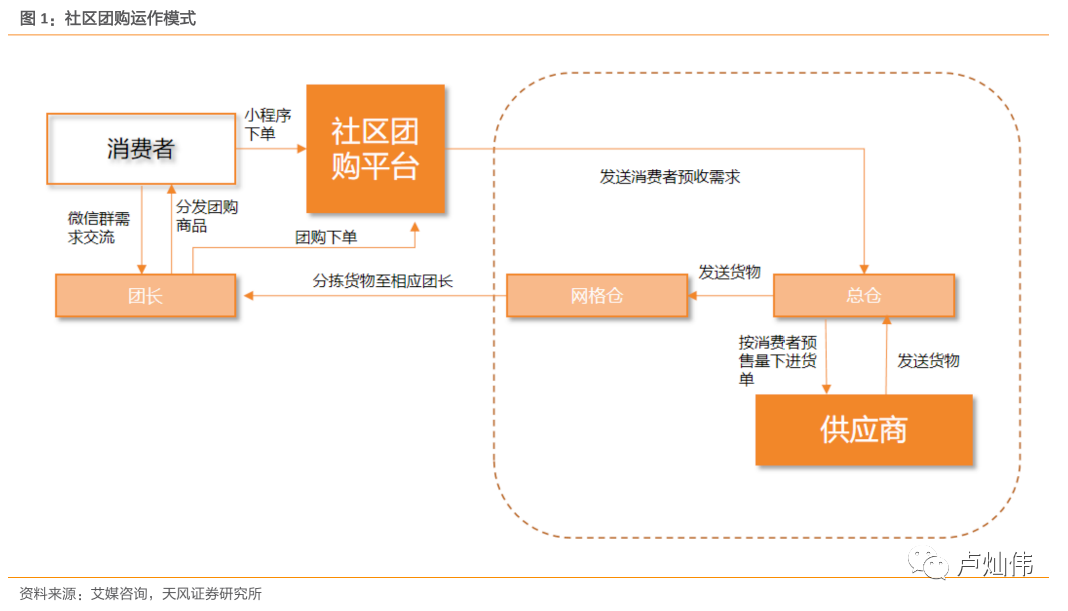

First of all, community group buying is a consumption model that takes residential communities as units and conducts group buying sales through channels like WeChat Moments and WeChat groups, providing daily necessities and life services for community residents.

Differences from Existing Scenarios

Difference from WeChat Business

Many people think, isn't that just WeChat business?

In fact, the essence of acquiring traffic is the same; it's just that WeChat business's private domain traffic comes from people all over the place.

Community group buying, on the other hand, targets the neighborhoods around you.

In terms of the model, WeChat business resells goods from upstream sources, which may come from suppliers or directly from factories. In most cases, they do not stock goods but rely on upstream direct shipping.

Community group buying also involves goods from upstream sources, but in most cases, the upstream is the community group buying platform, and the goods are sent to a unified location for users to pick up.

WeChat business is more retail-oriented, while community group buying is more wholesale-oriented.

Difference from Group Buying

When it comes to group buying, everyone must think of Pinduoduo, or rather, it should be called "Pindaddy," as the billions in subsidies are indeed attractive.

The group buying model requires a certain number of participants to successfully complete a payment. However, for most products, it usually only takes two people to form a group. So far, I have not encountered a situation where a group could not be formed, which means that group buying products must have a limited number of SKUs. You can see that each store on Pinduoduo generally has around 10 SKUs, and there is a certain overlap in SKUs among different merchants to ensure bargaining power with suppliers.

Group buying essentially attracts customers through low prices to generate popularity and sales, and there won't be too many SKU choices.

Difference from Traditional Group Buying

As mentioned earlier, traditional group buying attracts customers through low prices, and community group buying does the same. However, the user groups are not necessarily the same; community group buying targets user groups based on neighborhoods, and the consumption model is basically the same, transitioning from online traffic to offline. The slight difference is that community group buying products are uniformly provided by the community group buying platform, while traditional group buying is more focused on providing products from individual merchants.

Difference from Fresh E-commerce

Here, fresh e-commerce mainly refers to platforms like Hema and Dingdong. The biggest difference between this type of e-commerce and regular e-commerce lies in time. When purchasing fresh produce, we can go to Taobao or JD.com, but we have to wait for days, which is particularly uneconomical for products with high spoilage rates like fresh produce.

Later, the concept of integrated warehouse-store e-commerce emerged, which we previously mentioned as Hema Fresh. The emergence of integrated warehouse-store significantly reduces losses during logistics and transportation and can provide more SKUs. For instance, Hema Fresh offers nearly ten thousand SKUs and can achieve delivery within one hour.

The problem with integrated warehouse-store e-commerce is that it can only cover most areas. For example, the place I used to live was not covered, just a kilometer or two away. This led to the emergence of platforms like Dingdong, which increase regional coverage by reducing SKUs and adopting a pre-storage model.

However, whether it's integrated warehouse-store e-commerce or the pre-storage model, their inventory cycles are around 1.5 days, meaning that if products do not sell, there will be losses. For example, brands like Qian Dama and Yonghui Supermarket will discount products after 8 PM, but this model is a double-edged sword, meaning that it delays the opportunity for full-price sales to discounted sales, further compressing profits. In cases of poor management, some franchisees may take risks to sell expired products, damaging the brand.

So, is there a way to reduce the inventory cycle without having to wait so long? That would be through pre-sales and centralized pickup, which is community group buying. By accumulating a large number of orders through pre-sales, logistics can be unified to each pickup point. Although most platforms promote "order today, pick up tomorrow," the fulfillment duration for most community group buying platforms is actually between 6 to 12 hours.

Development of Community Group Buying

Before discussing development, let's first explain the community group buying model. Community group buying platforms recruit group leaders and suppliers. Group leaders are mainly responsible for sales, receiving and sorting goods at pickup points, and after-sales service. Suppliers settle on the community group buying platform, and after consumers place orders, suppliers deliver the goods to the community group leader the next day based on order volume, and consumers go to the pickup point to collect their goods, with group leaders earning commissions.

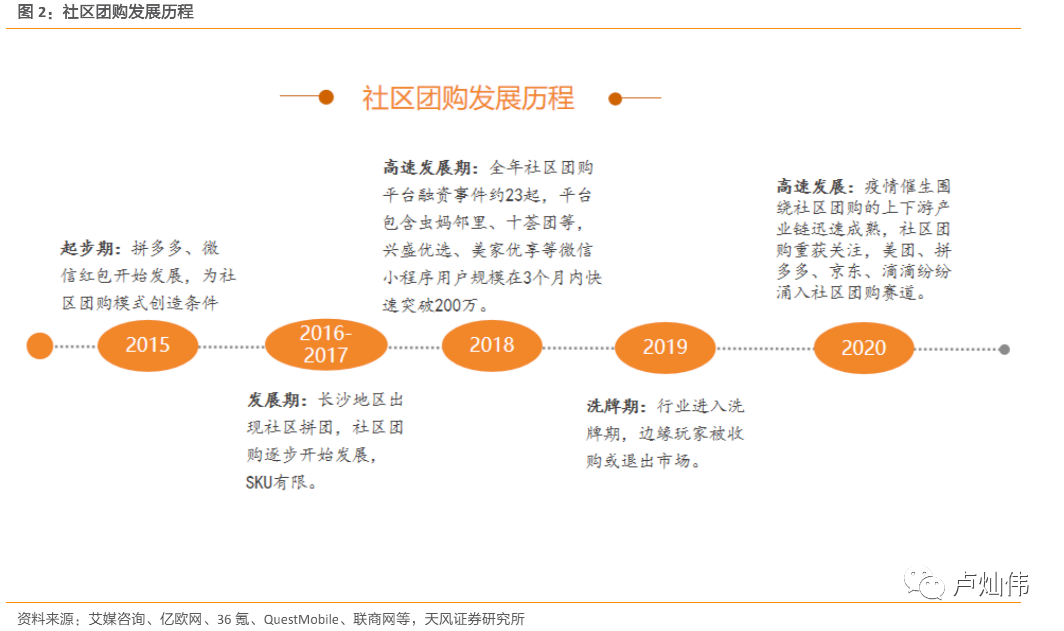

In 2015, mobile payments began to develop, followed by the rise of fresh e-commerce, which needed to expand due to cold chain logistics. A representative example is SF Best, while Tongnian Xingsheng relied on offline stores, where store owners delivered goods to consumers.

In 2016, community group buying began to appear in Changsha, followed by the development of the pre-storage model, with familiar names like Meiri Youxian and Dingdong entering the scene, attracting customers through subsidies and building their own warehouses and delivery teams.

By 2017, the SKU categories in community group buying began to expand, and the supply chain logistics infrastructure started to mature.

In 2018, major players entered the market, with around 23 financing events that year.

In 2019, the industry underwent reshuffling and reorganization.

In 2020, the pandemic accelerated the development of community group buying, with Meituan, Pinduoduo, JD.com, and Didi all entering the market.

As mentioned earlier, Hema's SKUs are around ten thousand, Dingdong's are about 1500, Meiri Youxian's are around 3500, while community group buying SKUs range from 500 to 1000, depending on the size of the warehouse and the inventory cycle. Community group buying has low traffic costs and low average order values, with average order values being about half of those in traditional fresh e-commerce (which was once referred to as new retail but is now considered traditional fresh e-commerce).

Advantages and Risks of Community Group Buying

In fact, the biggest problem community group buying solves is the pain point of fresh produce spoilage. Pre-sales and zero inventory significantly reduce turnover risks and inventory turnover risks, preparing as much stock as there are orders.

If you have read "The Tim Cook Biography," you would know that Apple's current valuation of $2 trillion is not solely due to Steve Jobs; Tim Cook is often credited with saving Apple. At that time, Apple was on the brink of bankruptcy, and Jobs had just returned to the company without having sold any products. The only notable thing was the "Think Different" advertisement. The biggest problem Apple faced was the inventory backlog of PowerBooks, which caused significant losses, and they underestimated the demand for the new Power Macs, leading to overly conservative production orders and ultimately resulting in severe shortages. Later, Jobs found Cook, who was working at Compaq. After Cook joined, he reduced the product inventory cycle from 30 days to 6 days, and later to just 2 days, ensuring that factory production matched immediate demand.

In the past, merchants had to bear greater risks to manage inventory themselves. Now, the risk of goods is borne by the community group buying platform, which naturally means that corresponding profits will also decrease. Community group buying platforms can continuously optimize product selection, logistics, and warehousing through big data, further lowering product prices, allowing consumers to purchase goods at even lower prices.

Due to the low price and low cost characteristics of community group buying, it can only cover third- and fourth-tier cities. Currently, the highest penetration rates are concentrated in prefecture-level and county-level cities, while penetration in towns and villages is relatively low. This is mainly due to the local cold chain and logistics systems being underdeveloped, which limits the growth of regional fresh e-commerce.

A core aspect of community group buying is the group leader, which is somewhat similar to live-streaming hosts. Currently, the entire community group buying sector is still in a phase of wild development, with group leaders primarily working part-time, most of whom are store owners transitioning from existing offline stores, and traffic primarily comes from the private traffic of group leaders. Once a team switches platforms, it brings a decline in traffic.

Fresh e-commerce cannot offset the costs of warehousing, so without considering R&D management fees and traffic costs, a scale of at least 1500 orders is needed to offset warehouse costs. Community group buying, however, can achieve profitability with just 500 orders.

Additionally, because it involves warehousing, fresh e-commerce requires site selection, decoration, and pre-storage, making it a relatively heavy model. Community group buying does not require this, making the overall model lighter and allowing for rapid replication.

Community Group Buying Battlefield

Xingsheng Youxuan

Xingsheng Youxuan is currently a leading player in community group buying, with a clear first-mover advantage. It has been deeply rooted in localization for many years. From the situation in Wuhan, paper bowls hold a status equivalent to that of eggs in fresh produce; currently, only Xingsheng Youxuan places paper bowls at the top of its category.

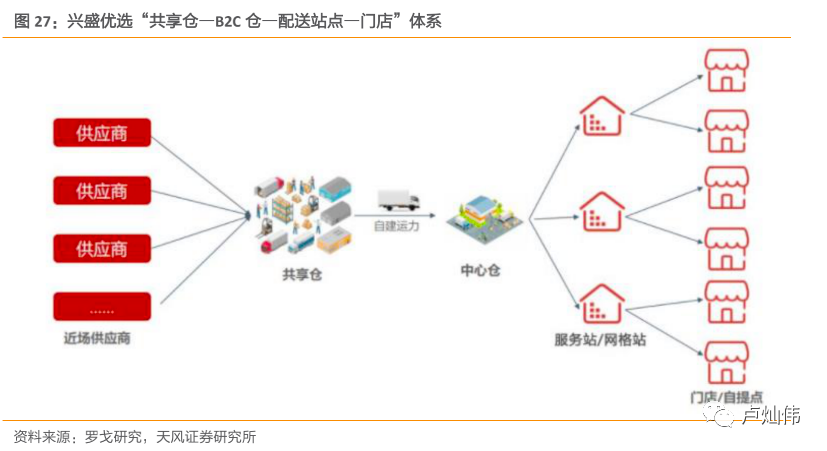

Xingsheng Youxuan has over 300,000 stores nationwide, with 8,000 to 10,000 new stores opening each week. The group leaders are primarily store owners, meaning Xingsheng Youxuan has over 300,000 group leaders. The parent company of Xingsheng Youxuan started with convenience stores and has a very well-established supply chain. Since 2016, it has been experimenting with O2O (Online to Offline). The logistics structure of Xingsheng Youxuan consists of a four-level logistics network model: "shared warehouse - B2C warehouse - distribution station - store."

Behind it is Tencent, which provides certain support and inclination in terms of traffic. Although there are 300,000 group leaders, whether they can withstand the competition from seasoned players like Meituan and Pinduoduo for talent is a significant variable.

Shihuituan

Last year, Shihuituan merged with "Niwo Nin," entering the top tier of the market, reminiscent of the merger between Didi and Kuaidi back in the day, with Alibaba backing it. It currently has 100,000 communities and differs from Xingsheng Youxuan in its model, adopting a three-tier warehousing logistics system: "regional warehouse (shared warehouse) + city warehouse (distribution warehouse) + service station."

Alibaba has upgraded all offline retail stores under its Retail Link to pilot community group buying businesses for Shihuituan, and has also turned the heads of Cainiao stations into community partners for Shihuituan. Alibaba provides significant support in supply chain, operations, and traffic.

Meituan Youxuan

Meituan has more experience in operations and ground promotion than the previous two players, but it started late in warehousing and has less experience in community management. However, it has a more comprehensive ecosystem. Meituan Maicai focuses on super first-tier cities, Meituan Shanguo targets quasi-first-tier or second and third-tier cities, while Meituan Youxuan is aimed at sinking markets. Currently, WeChat also provides support for traffic entry.

Duoduo Maicai

Pinduoduo is most familiar with the sinking market battlefield, and its brand is already favored by users. Merchants on Duoduo Maicai can choose to become Pinduoduo merchants, and vice versa. However, its shortcomings are also evident, lacking its own logistics channels and relying on third-party supply chains.

Chengxin Youxuan

Didi has excellent scheduling and ground promotion capabilities, and can draw on previous experiences with car owners for managing group leaders. However, its shortcomings are clear: it has no experience in community e-commerce, inconsistent user demographics, and currently targets mainly first-tier city populations. Huaxiaozhu is also investing heavily to expand its user base in sinking markets, with no upper limit on investment for user acquisition. Currently, Didi leads in daily orders among community group buying platforms, with Xingsheng Youxuan at around 5 million daily orders, while Chengxin Youxuan has surpassed 7 million daily orders.

Alibaba and Tencent

Community group buying essentially exists as a business model built on WeChat infrastructure. Meituan, JD.com, Pinduoduo, and Tencent all hold around 18% stakes, including new players like Xingsheng Youxuan and Shihenghui. Tencent's advantage lies in traffic, but in other aspects, all companies are weaker than Alibaba. It can be said that Alibaba has comprehensive advantages beyond just traffic entry, with a large number of Cainiao stations in offline stores, a powerful logistics network, and strong supply chains like Hema Fresh and RT-Mart. However, doing business within WeChat's ecosystem poses certain challenges.

Other Players

During the pandemic, community group buying became one of the growth drivers for property management companies. Country Garden plans to launch "Biyouxuan" in 2020, aiming to establish over 600 locations in the Greater Bay Area. Property management companies have several advantages, such as self-pickup points, fewer trust issues, owner groups, and data on residents' purchasing power. However, their disadvantages are also apparent, as they lack a supply chain system.

Some Views

Currently, it seems to be a competition between traffic and supply chains. With Pinduoduo becoming the second-largest e-commerce platform, it appears that traffic will ultimately be key.

In March 2020, Guosheng Securities released a report analyzing Pinduoduo's "full value chain," indicating that the cost of the entire channel (i.e., the cost of goods flowing from this channel to consumers) is 23.8% for Pinduoduo, 12.8% for Alibaba, and 15.2% for JD.com.

Alibaba's supply chain costs are lower than those of Tencent's players. Whether the bargaining power of traffic can offset channel costs is a question worth discussing.

Can the entry of property management companies change the game? At least from my perspective, it seems unlikely. Observing the development of property management companies and Cainiao stations shows that the future development of Cainiao stations will definitely be local service points within communities.

Since the People's Daily commented on it, community group buying seems to have become the original sin of the giants, with various rumors circulating that major players are launching community group buying initiatives. Comparisons have been made between community group buying and P2P lending, long-term rentals, and the pressure on market vendors. Firstly, I believe that those who spread these views are either bad or foolish, often using terms like "the common people" or "the country" to label businesses. Anyone seeing such extreme views from seasoned professionals or entrepreneurs might consider unfollowing them.

The reason we have so much innovation is due to the immense tolerance for new things. A new business model will inevitably have many problems, followed by various regulatory policies. Issues like designated parking areas for shared bikes and the crackdown on second-tier payment companies are examples.

Capital is not foolish either; businesses are divided into two types: traffic-based and commercial. Some products may not be profitable on their own and may even incur losses, but they can drive significant traffic to other businesses, thus achieving profitability. Commercial products may not have much traffic resource but can realize profits through strong monetization capabilities.

Currently, community group buying holds advantages in both aspects. Whether it will develop into a commercial or traffic-based business in the future is still uncertain, but it will definitely require a footprint.

In the process of establishing a footprint, some existing groups under previous models will inevitably be harmed. The most common example is the direct squeeze on traditional markets, using subsidies and a strong supply chain to sell vegetables at unreasonable prices. There are also issues of excessive expansion leading to management failures, such as customers going to pick up goods the next day and finding they cannot get the vegetables they bought for one cent yesterday. Similar problems are likely to be numerous, but the entire ecosystem will gradually become healthier.

However, consumers are loyal to prices. Take live streaming as an example: if Li Jiaqi cannot offer the lowest price online, setting aside loyalty, would you still place an order with him or go to the neighboring live stream for the lowest price?

As for whether offline markets will be completely driven out, I believe they will not. Offline scenarios still have their significance. Just as e-commerce has not eliminated supermarkets and ride-hailing has not replaced taxis, it is certain that some will struggle to survive, accelerating the transformation of traditional markets.

Let’s think outside the box: in the future, markets may become warehouses for specific areas, with more customers coming from various platforms and offline stores rather than the current retail model. I believe that ultimately, under a new model, they will find their new ecological niche.

As consumers, we are currently enjoying the benefits of low-priced goods in the subsidy war. As store owners and part-time group leaders, we enjoy subsidies of several or tens of yuan per order.

Alternatively, one might consider investing in stocks of Pinduoduo and Meituan, or their backers Tencent and Alibaba.

Reference Sources:

Community Group Buying: The Resurgence of the Sinking Market, A Battle Among Giants

Qing Shiwuwu: Understanding Community Group Buying in One Article

Previous Articles:

The Next Generation Note-Taking App Notion: How I Use It to Manage Knowledge

How to Improve Cognition?

Let’s Talk About Interviews and Recruitment.